Hi ,

The information you have provided is as follows:

Three year average income:

Participant’s age:

A participant with the above mentioned parameters can accumulate

(Lump Sum at Retirement Amount) till he reaches an assumed retirement age of (Retirement Age) . In the first year, a maximum contribution of (Maximum Contribution) can be made to the plan.

A plan can be incorporated at any time during the year, and within a certain time in the following year. The funding of the defined benefit plan can also happen any time before the company files its tax returns.

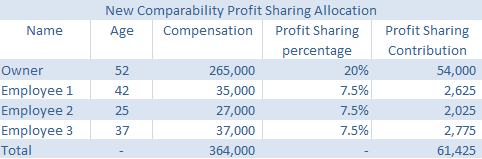

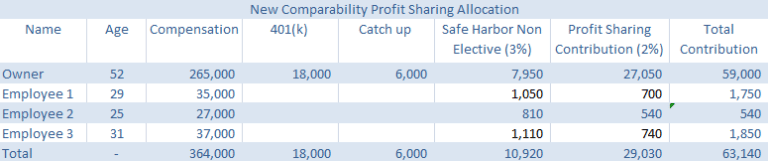

If you have employees, the IRS mandates you to make available a retirement plan for employees as well. Depending on the plan design, you will be required to contribute an amount of 3% to 7.5% of the employee wages in a profit sharing plan. We will consult with you to come up with the best plan design based on your circumstances and company demographics. Our Census Request Form will be emailed to you which has to be filled and sent back to info@pensiondeductions.com .

Please enter your email address below. A comprehensive report shall be emailed to you outlining the further steps you need to take in order to get started with a defined benefit plan.

Please note that these contribution amounts are approximate amounts and only for the first year of the plan. These amounts still need to be certified by an actuary and contributions should not be made based only on the amounts generated by the online calculator without consulting an actuary.