Explore the difference between a Pension Plan and a 401(k)

Retirement planning is crucial for securing financial stability in later years, and two popular options in The USA are pension plans and 401(k) plans. Though both are designed to support individuals in building their retirement savings, they function very differently. This blog explores the difference between a Pension Plan and a 401(k), highlighting how they work, their benefits, and which may be a better fit for your needs.

What is a Pension Plan?

A pension plan, also known as a defined benefit plan, is an employer-sponsored retirement plan that promises a fixed monthly benefit to employees after retirement. The amount is typically calculated based on factors such as the employee’s salary, age, and length of service. The employer is responsible for funding the plan and managing the investments. Upon retirement, the employee receives a guaranteed income for life, which makes this a secure and predictable option.

Understanding the difference between a Pension Plan and a 401(k) helps individuals make more informed decisions about their retirement options.

Understanding the difference between a Pension Plan and a 401(k) helps individuals make more informed decisions about their retirement options.

What is a 401(k) Plan?

A 401(k) plan is a defined contribution plan, primarily funded by the employee through payroll deductions. Employers may offer matching contributions but are not obligated to do so. The contributions made into a 401(k) plan are typically pre-tax, lowering the participant’s taxable income for the year. The employee controls how the funds are invested, usually by choosing from a range of mutual funds. The amount available at retirement depends on the total contributions made and the performance of the chosen investments.

The difference between a Pension Plan and a 401(k) becomes clearer when we look at the flexibility and control each plan provides. While pension plans are largely employer-driven, 401(k) plans give employees more autonomy over their retirement savings.

The difference between a Pension Plan and a 401(k) becomes clearer when we look at the flexibility and control each plan provides. While pension plans are largely employer-driven, 401(k) plans give employees more autonomy over their retirement savings.

Know More!

Schedule a Free Consultation Now!

Schedule a Free Consultation Now!

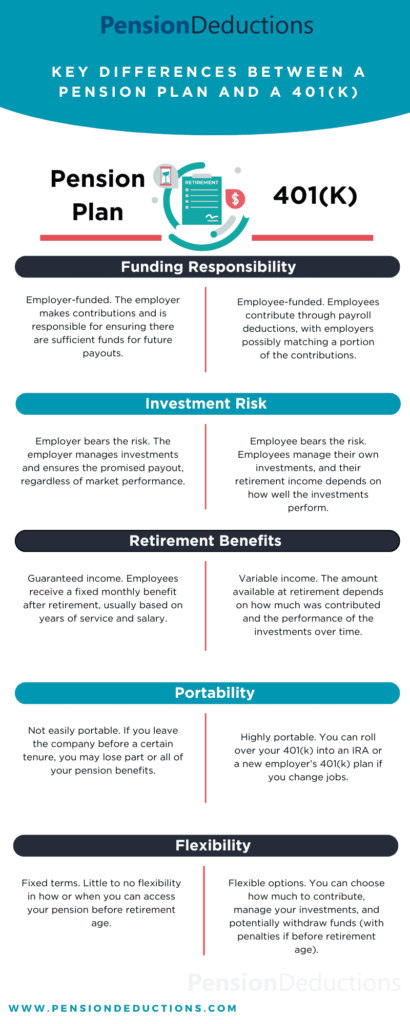

Key Differences Between a Pension Plan and a 401(k)

There are several key differences between a Pension Plan and a 401(k) that significantly affect how employees approach retirement savings. Let’s break them down:

Funding Responsibility

| Pension Plan | 401(k) |

|---|---|

|

The employer takes on the responsibility for funding the pension plan, making contributions based on actuarial calculations |

The employee is primarily responsible for contributing to their 401(k), although employers may contribute matching funds |

This difference between a Pension Plan and a 401(k) affects how retirement income is funded, with pension plans relying more on the employer and 401(k) plans putting the onus on the employee.

Investment Risk

| Pension Plan | 401(k) |

|---|---|

|

The employer bears all the investment risk. If the investments underperform, the employer is still required to meet the promised payouts |

The employee bears the investment risk. Poor investment choices or market downturns can significantly impact the value of the 401(k) account |

The difference between a Pension Plan and a 401(k) in terms of risk is substantial, as pension plans provide more security while 401(k) plans offer more flexibility but with greater financial uncertainty.

Retirement Benefits

| Pension Plan | 401(k) |

|---|---|

|

Pensions provide a guaranteed income stream for life, ensuring financial security regardless of market conditions |

The amount available for retirement depends on how much was contributed and how well the investments performed |

This difference between a Pension Plan and a 401(k) shows that while pension plans offer stability, 401(k)s may offer higher potential returns but with added risk.

Portability

| Pension Plan | 401(k) |

|---|---|

|

If an employee leaves a company before reaching a certain tenure, they may not receive full pension benefits. Pensions are less portable because they are tied to the employer |

A 401(k) is portable. Employees can take their 401(k) account with them when they switch jobs, either rolling it over into a new 401(k) or an individual retirement account (IRA) |

The difference between a Pension Plan and a 401(k) in terms of portability is crucial for those who expect to change jobs frequently.

Tax Considerations

Tax implications play a significant role in the difference between a Pension Plan and a 401(k). Both options offer tax-deferred growth, but there are differences in how and when taxes are paid.

| Pension Plan | 401(k) |

|---|---|

|

Pension contributions made by employers are tax-deductible for the employer. Employees pay taxes on the pension benefits when they are received in retirement |

With a traditional 401(k), contributions are made pre-tax, reducing taxable income. Taxes are paid on the distributions during retirement. In a Roth 401(k), contributions are made with after-tax dollars, but withdrawals in retirement are tax-free |

Which is Better: Pension Plan or 401(k)?

Choosing between a pension plan and a 401(k) depends on your personal circumstances and preferences. For those who prioritize financial security and predictability, a pension plan may be the better choice due to its guaranteed income. However, pension plans are becoming rarer, especially in the private sector. On the other hand, a 401(k) offers more control and flexibility but requires employees to manage their own investments and shoulder the risk.

Understanding the difference between a Pension Plan and a 401(k) is critical for making informed retirement decisions. If your employer offers both options, carefully evaluate your financial situation and retirement goals to determine which plan best suits your needs.

Understanding the difference between a Pension Plan and a 401(k) is critical for making informed retirement decisions. If your employer offers both options, carefully evaluate your financial situation and retirement goals to determine which plan best suits your needs.

The Future of Pension Plans and 401(k)’s

In recent decades, there has been a significant shift away from pension plans toward 401(k) plans, especially in the private sector. The cost of maintaining pension plans has led many companies to phase them out in favor of 401(k) options. However, pensions remain common in the public sector, including for government employees, teachers, and union workers.

Understanding the difference between a Pension Plan and a 401(k) will help you navigate this evolving landscape and make the best decision for your retirement future.

Understanding the difference between a Pension Plan and a 401(k) will help you navigate this evolving landscape and make the best decision for your retirement future.

Conclusion

Understanding the difference between a pension plan and a 401(k) is crucial for making informed retirement decisions. Pension plans offer guaranteed income and employer responsibility, while 401(k) plans provide more flexibility and control but place the investment risk on the employee. Your choice will depend on your risk tolerance, job stability, and the options available through your employer. Both have their advantages, and the right choice depends on your individual retirement goals and financial situation.

For more personalized advice on which plan is right for you, consult with a financial advisor to ensure you’re making the best choice for your future.

For more personalized advice on which plan is right for you, consult with a financial advisor to ensure you’re making the best choice for your future.

SHARE THIS POST

Related Blogs

Defined Benefit Plan vs 401k: Best Pension Plans for Small Business Owners

Read More »

Discover the key differences between a Defined Benefit Plan vs 401k, and find the best pension plan for small business owners.

Shrideep Murthy

February 25, 2025

2:48 pm

Retirement Trends to Watch in 2025

Read More »

Explore the latest Retirement Trends in 2025, including 401(k) updates, automatic portability, and inflation-resistant strategies, to secure your future.

Shrideep Murthy

January 2, 2025

9:15 pm

3 Retirement Rule Changes in 2025

Read More »

Discover the 3 retirement rule changes in 2025, including contribution limits, RMD updates, and automatic portability. Plan smarter today!

Shrideep Murthy

December 24, 2024

9:15 pm

Year-End Financial Planning in the USA

Read More »

Year-end financial planning in the USA helps optimize retirement savings, reduce taxes, and secure your future with proactive strategies.

Shrideep Murthy

December 17, 2024

9:15 pm